When an ordinary people talk about the account, they generally mean the account for transactions in the bank. However, in the world of business, it has an entirely different meaning and is related to the subject of accounting where all the transactions are maintained in a structured by an expert who is also known as the accountant. They keep all the records of the debits and the credits and provide the financial status of the company at any given point of time showing if the business house is running at a profit or a loss. However, this is a generalized outlay of account, but one can also go deep into the subject and learn in-depth.

If we go by definition, keeping of the records with the help f the total accounting system that can help to keep track of all the activities related to finance like the revenues, expenses, equity, assets, and the liabilities. The records change from time to time and almost daily as the business activities of a company change. The financial operations are stored by the accountant in a ledger for the preparation of the financial statement as and when required or at the end of the period of accounting.

What is a Debit and Credit in Accounting?

As an accountant prepares the financial statements, the balance sheet is the topmost sheet showing the overall financial condition of the business. Then comes the assets followed by the liabilities, stockholders, or the owner equity, the revenue or the income, expenses, gains, and finally the loses. However, the two corner stone’s of accounting is debit and credit without which n accounting statement can be prepared.

- The Debit in Accounting

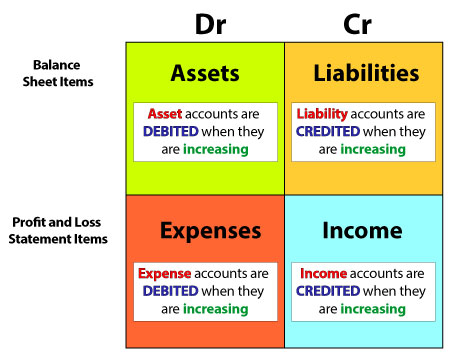

Debit in accounting is the use of value while a transaction is taking place. It is the way by which an accountant can express the ups and downs of the expenses and assets or the incomes and liabilities in terms of money. It is the first account entry recorded in the journal and always presented on the right side of the ledger account. If we go by the equation, it is nothing but Liabilities added with equity to give the assets that are reflected after debiting a single account. However, under the double-entry system of accounting, debit is not enough to balance the total transaction.

- The Credit in Accounting

By the meaning of credit in accounting, an accountant means to value for the source for making any transaction. It is the method by which the accountant reflects the ups and downs in the incomes and liabilities, and the assets and the expenses in monetary terms. It is always recorded after the debit entries in the journal and is suffixed by the word “To” which is followed by the respective head. It comes on the right side of the ledger, and again if we go by the equation, we can say assets are equal to liabilities and the equities and are credited from one account. Yet credit is also dependent on debit as it cannot balance the complete transaction without the help of the debit account.

What is Debits and Credits in Double-Entry Accounting?

The double entry account system is the general norm to prepare a correct financial statement and is practiced almost by all accountants throughout the globe. It is a systematic and organized pattern to maintain any transactions in the accounting system. It means that any entry that is made in the books of the accounts will at least have two parts to balance the statement and one part will come under the assets side and the other part on the liabilities side. The result of the outcome is, therefore, precisely equal and opposite. It is necessary to make a correct balance sheet where the total asset of a company is equal to the total liabilities plus the liabilities. Without recording the debits and credits, it is not possible to make a proper balance sheet so that both the sides are equated.

Balances of Accounts: What is a Debit Balance and a Credit Balance?

In an account statement, the difference between the debit and credit side is known as the balance. It can be positive, as well as negative. When the total debit side is more than the sum total of the credit side, the figure represented is known as the debit balance, and if it is on the reverse, then it is called the credit balance. The common man has an idea that the credit balances are good and the debit balances are bad, however, if we consider revenue earnings it is always good as the expenses incurred decreases the net income but the pun is that in the balance sheet the liabilities are shown in the credit side and the assets are shown on the debit side. Both are the building blocks for accounting purposes and cannot be said that either of them is bad or good.

Which types of accounts normally have debit balances, and which have credit balances?

Expenses, assets, the owners’ drawings, and the losses are known as the debt balances. With each debit entry of these types, the debit balance will increase, and the credit balance will decrease. Again, on the other hand, revenue from sales, liabilities, equity of the owners, gains, and the equity accounts of the stockholders come under the credit balance. The balance increases as the account are credited and decrease as it is debited.

Conclusion

Thus, we can conclude that without keeping proper records of any transaction in the ledger and the book of accounts, it is impossible to have a deep insight into the financial position of any business entity. Accounting properly with the entries on the correct side helps to finalize the balance sheet and give an overview of the company. It is the job of the accountant to record all transactions and maintain the book of accounts to gauge the financial status of the company and propel the business entity in the right direction and make correct decisions.