A bookkeeping worksheet is prepared, traditionally at the very end of the entire reporting period, which keeps the balances of every ledger and is then compiled into credit and debit column totals, which are equivalent. This worksheet is known as a trial balance. Many companies use this balance at intervals to make sure that the entries made in their bookkeeping system are measured and mathematically correct. Not only that, but this also helps the companies keep records and ensure that no entry goes unnoticed.

Apart from the basic aid, a trial balance is important for a lot of other reasons as well. Preparing one for a company helps them detect if there is some mathematics error in the double-entry accounting system. A trial balance is said to be balanced only if the total credits equal to the total debits. However, this won’t be possible if there are any mathematical errors in the ledgers. But there can still be a few errors in the company’s accounting system. For instance, many transactions are sometimes missing from a system or may be classified incorrectly. This could be considered as material accounting errors, however, would not get detected by this procedure of trial balance.

What Does a Trial Balance Includes?

To calculate a trial balance, a company needs to have certain information at hand. Further mentioned below is some of the information a company needs to calculate the trial balance:

- Ledger accounts:

Every transaction of a company is initially recorded within the bookkeeping accounts of a general ledger. However, depending on what type of transaction has occurred, companies can find if the ledger accounts are credited or debited in the bookkeeping period before they are put together to calculate the trial balance. On top of that, some of these accounts might have been used to keep track of several business transactions. Accordingly, like the trial balance worksheet shoes, the balance at the end of every ledger account is the total of all credits and debits that were entered. These accounts make a note of only business-related transactions.

- Credits and debits:

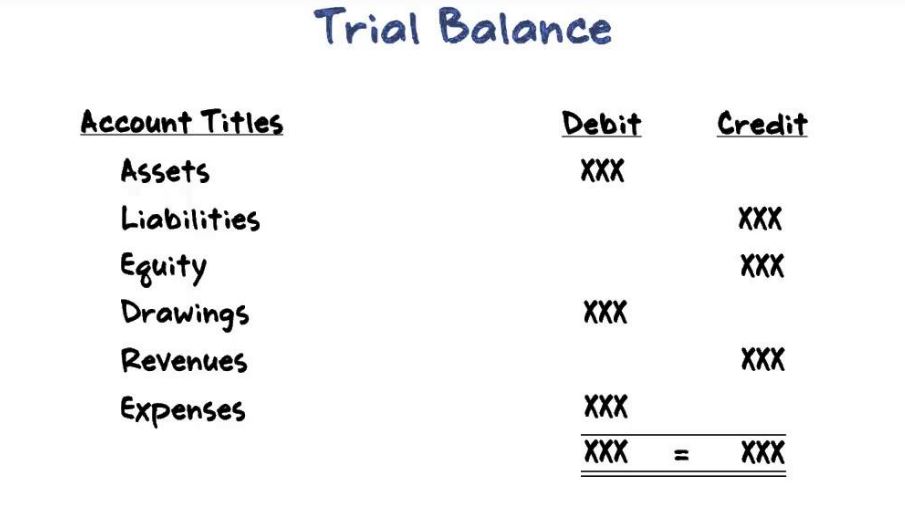

When the accounting period of a company is about to end, the loss or expense and all accounts of the asset should have a debit balance, while the equity, accounts of liability and gain or revenue should have a credit balance of their own. Nevertheless, some former accounts may also have been credited while to specific accounts of the second type might have been debited all through the accounting period. Such a reduction of credit and debit balances of certain related business transactions can have an opposite effect on the respective accounts’ final credit and debit balances. On a trial balance worksheet, the debit balances are written on the left column and all of the credit balances on the right column. Along with the transactions, the account titles are mentioned to the far left of both columns.

What are the Errors Occurs in Trial Balance?

Although the trial balance worksheet is the best way to calculate the transactions of companies, there might be some unforeseeable errors that might occur. After every ledger account and their balances have been listed on a trial balance worksheet in the standard format, all the credit balances and debit balances are added up separately to prove that the total credit and debits have the same value. Since this calculation involves a lot of uniformity, it guarantees that there will be no unequal credits or debits that would be entered incorrectly in the process of double-entry recording. Mentioned below are few of the common errors of this report:

- An error of oversight: Sometimes, a transaction might not be entered in the system.

- Reversal error: There might sometimes be cases where the account that has to be debited s credited and vice versa. This can further cause discrepancies in the result.

- Original entry error: This process of double-entry transaction sometimes includes wrong amounts on both debit and credit columns.

However, there is another shortcoming of this process. Since the trial balance cannot detect any bookkeeping errors apart from simple mathematical mistakes, if equal credits and debits are submitted in wrong accounts, or if offsetting errors are with simultaneously with a credit and debit or a money transaction is not listed, the trial balance worksheet will still provide a perfect balance between the total credits and debits.

What is the Purpose of a Trial Balance?

There are many reasons why to why a trial balance worksheet is used to calculate ledger balances. Further mentioned below are some functions and advantages of trial balance:

- It offers a businessman a comprehensive list of all the ledger balances.

- It is one of the shortest and quickest methods of verifying and calculating the mathematics accuracy of inputs in the ledger.

- It the summation of the debit side column and the summation of the credit side column are equal; the trial balance is considered to be correct. However, if they differ, there is said to be some errors made in the preparation of the accounts.

- It is also very helpful in the process of preparing the final accounts, like Profit and Loss account, Trading account and Balance Sheet.

Examples of Trial Balance:

A trial balance is mainly considered to be an internal report that can be useful in the manual accounting system and is not a financial statement. If the calculation did not match, there is said to be an error between the trial balance and the journal submitted. There can be many reasons that can lead to such a miscalculation in the account balance. However, most of the times, the reason behind such a miscalculation is posting a credit amount as the debit amount or vice versa. Apart from that, preparing a trial balance or transposing digits within the amount while posting it can be some other reasons as well.

Such an efficient method of calculation can help companies make sure their calculations are correct. This can further help the companies be certain that no losses are incurred.