There were minimal options available for you if you were looking for investment instruments in the past. However, times have changed drastically. The market is littered with great investment plans. With such a wide range of options available for individuals, it becomes quite difficult for individuals to pick a single plan out of them.

Two of the most sought after products in the market are Unit-Linked Insurance Plans (ULIPs) and Equity-Linked Savings Schemes (ELSS). While both the plans are quite lucrative, they have certain differences. If you’ve decided to opt for one of the two, you will need to understand your financial objective and goals first. Let’s understand the plans individually.

What are Equity Linked Savings Schemes?

ELSS plans are basically diversified equity mutual funds. This scheme invests in the market and opts for companies with different market capitalizations. The plan comes with a minimum lock-period of 3 years. Investors willing to invest in the plan can make the payments either through SIPs or submit a lump sum amount to earn the benefits. The returns can range between 14-20% annually, depending on the investment sum and market conditions.

Things to know about ELSS plans

Before investing in an ELSS, here are some points you can take a look at:

- You have the option of investing as much as you can in these plans. But investments of up to ₹1,50,000 are considered for tax deductions.

- It is the best tax-saving investment option, and it offers the advantage of tax deductions along with the chance to earn high returns within a short lock-in period.

- Long-term capital gains earned from ELSS plans are taxable.

- You can continue your investment in the plan even after it’s a mandatory lock-in period of three years is over.

- While the risks involved in ELSS plans are higher than PPFs or fixed deposits, the returns earned through these plans are high.

What are Unit Linked Insurance Plans (ULIPs)?

A ULIP plan will provide the investor with the dual-benefits of investment returns along with life insurance coverage. In a ULIP insurance plan, a part of the investor’s funds is used to provide the individual with insurance coverage, while the other part is used to invest in market instruments like debt, equity, hybrid, etc.

One of the benefits of selecting from the best ULIP plans for your investments is that you can switch between the investment instruments you have chosen during your plan’s tenure. This provides you with the ability to change your investment instrument based on whether they’re performing well or not. Also, you can shift between equity and debt instruments. If you feel the market is too volatile for you, you can shift to debt funds. Alternatively, if you want to capitalise on the high returns of the market by taking high risks, you can choose to go for equity funds.

Things to know about ULIPs

- They are quite different from the traditional investment policies as they offer you both insurance and investment together.

- The premium payments made towards ULIPs are kept for safeguarding the policyholder’s insurance needs and policy charges.

- Once these deductions are made, the policyholder pays the premium amount between the life cover and purchasing fund units for investment.

- The expenses involved in the ULIP investment will include administration charges, mortality charges, fund management charges, premium allocation charges, etc.

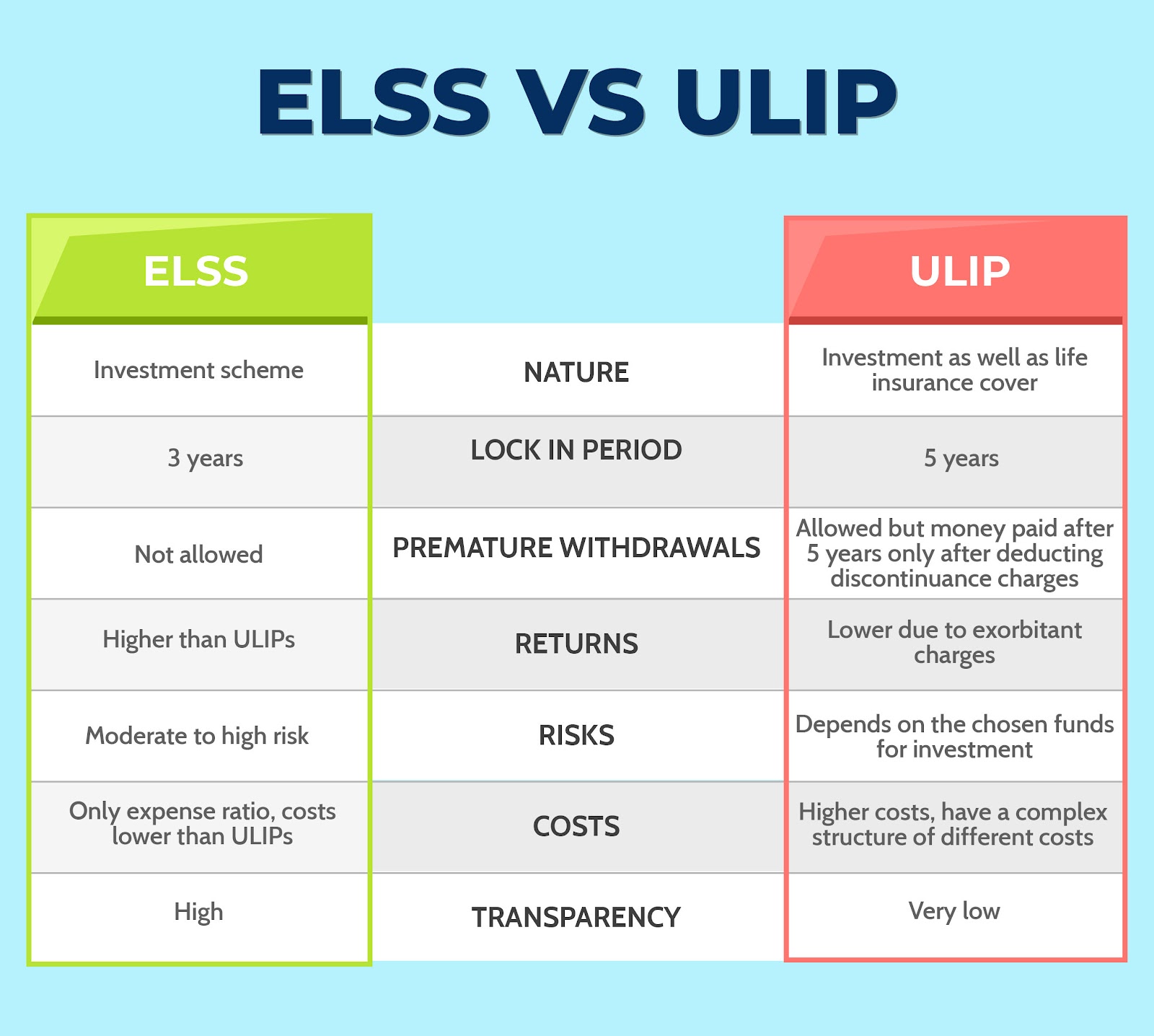

Comparison between both investment plans:

- ULIPs come with a compulsory lock-in period of 5 years, while ELSS plans have a mandatory lock-in of 3 years.

- ULIP returns can differ because the investor can select any combination of equity, debt, hybrid, etc. Since ELSS plans are market-linked, the returns will depend on the scheme chosen.

- In ULIPs, premiums paid are tax-deductible under Section 80C. Even for ELSS investments, the money invested can be claimed for tax deduction under Section 80C.

- For ULIPs, the maturity benefits are tax-exempt if the annual premium paid is less than ₹2.5 lakhs. If the premium paid is above ₹2.5 lakhs, the gains are taxed as Long Term Capital Gains (LTCG). For ELSS, the benefits, irrespective of the money invested, are taxable as LTCG.

- In ULIPs, the funds are available after a lock-in period of 5 years (along with policy conditions). In ELSS, the funds are available after a lock-in period of 3 years.

Hence, if you are looking for an investment tool that will provide you with tax benefits along with excellent returns, you must opt for ELSS plans. However, if you’re looking for a plan which will provide you with insurance benefits along with investment returns, then you must look for the best ULIP plans. Before choosing between the two, you must understand your objective and risk profile.