Prime Minister’s Employment Generation Programme

PMEGP stands for Prime Minister’s Rojgar Yojana and Rural Employment Generation Programme, which came into existence by merging PMRY(Prime Minister’s Rojgar Yojana) and REGP(Rural Employment Generation Programme) schemes with the purpose to make it easier for the beneficiaries/entrepreneurs to avail the loan with flexible terms and conditions, EMI options, and a convenient tenure of about 3-7 years with an added advantage to the subsidy provided by the central Government of India.

The PMEGP scheme aims to improve new employment opportunities for daily wage workers, craftsmen or artisans who go through difficult times when their skill set or work is not required due to the nature of business/markets they are involved in. Seasonal employment has been a huge concern for these workers for decades, which also tends to influence their migration to urban areas, developed states, and metropolitan cities to find sustainable employment opportunities.

As one might imagine that migrating to new places is a tough decision to take, but workers are left with no choice as it boils down to their survival. This indirectly has a huge impact on other established businesses as people migrating also happen to be customers to other businesses. As a result, enterprises also have to worry about the disparity in the labor rates as the supply side of workers shrinks.

PMEGP loan scheme is hence, intended to slow down the migration of these workers and, in turn, increases the cash flow, export products, and business functions, particularly in the rural parts of India, which will develop the unorganized sector as a whole. The scheme is actioned by the KVIC (Khadi and Village Industries Commission) boards at a National level and similarly implemented by KVIC boards, DIC(District Industries Centres) and banks at the state level.

Eligibility Criteria

- PMEGP loan applicants must be at least 18 years and above.

- Educational qualification is considered when the loan amount is more than 10 lakh or 5 lakhs for manufacturing and service sector businesses, respectively. Applicants need to complete schooling by the 8th standard.

- Established enterprises or those that have availed benefits from any other government schemes of a similar manner are not eligible to take benefits from PMEGP loan schemes.

- Charity trusts, Self-helpgroups and societies that are involved in production businesses.

- The scheme is only available for the creation of new entities/businesses and cannot be utilized by existing enterprises. Established SME/MSMEs can refer to the MUDRAscheme.

- Businesses should be situated in rural areas. A rural area or village is an area that is classified under the revenue records of the state. It also includes towns with less than 20,000 population.

- Industries in villages under the negative list depend on the surroundings and environments that are not suitable for such business activities.

- Business owners must invest a minimum of 10% of the total project cost, and SC/ST/OBC needs to contribute 5% of the total.

Benefits of PMEGP

There are numerous benefits of PMEGP loans over traditional loan options. The first and foremost benefit is the Government’s subsidy, which is known as “Margin Money” and has a lock-in period of 3 years. This money can be used after the lock-in period has expired, although banks make sure that you have exhausted the loan amount and require more money for working capital expenses as per the guidelines of the bank. The below table gives a clear picture of Margin-Money/Subsidy.

| Category | Subsidy | Subsidy |

| Area | Urban | Rural |

| General/OC | 15% | 25% |

| SC, ST and OBC, Physically challenged, Minorities | 25% | 35% |

- PMEGP also gives new business owners the ability to secure the loan upto 10 lakh without providing any collateral. The Government provides the collateral for loans of more than 10 lakhs to 25 lakhs.

- The scheme also covers an entrepreneurship development program that aims to provide 10 days to business owners taking loan amounts more than 10 lakh and 6 days for loans upto 5 lakhs. EDP training is mandatory and provides insights related to business operations, finance, management,and marketing. KVIC has well-equipped accredited training centres in many parts of India, and the Central Government provides funding.

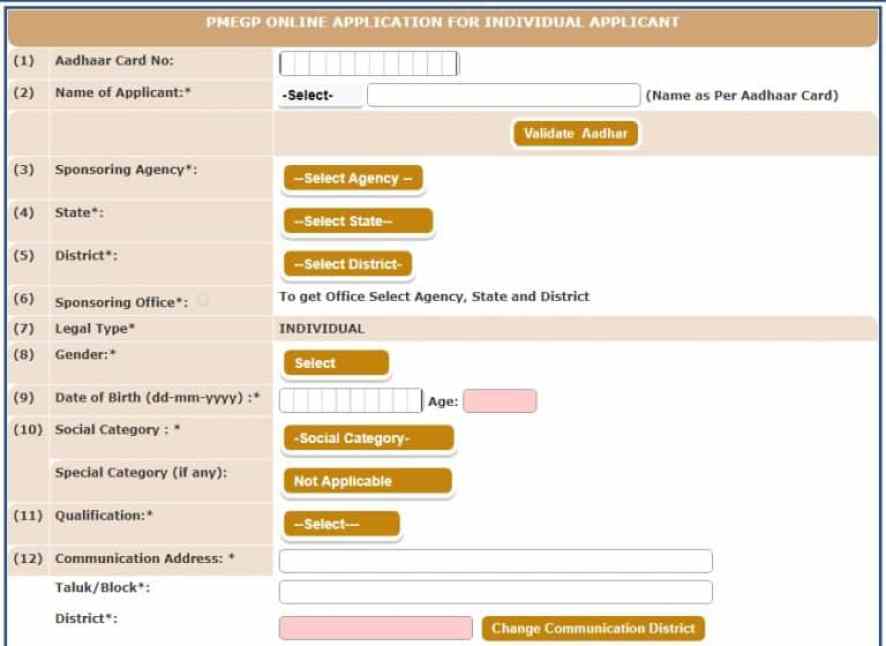

Steps to Apply

The online application process is quick and simple.Complete the following steps to apply:

- To apply for the PMEGP loan scheme, you must visit the PMEGP online portal and click on the PMEGP circle icon and then select PMEGP Portal, followed by the options ‘Online Application form for Individuals’ and ‘Online Application form for Non-individuals.’ Beware, there might be a different set of information required when submitting a non-individual application.

- Once the form is filled, scroll down to the bottom of the page and click the ‘Save Applicant Data’ button and make sure you upload all the necessary documents specified in the portal.

- Upon the submission of the application, you will receive an acknowledgment ID along with the password on your registered mobile number, with which the application progress can be tracked.

PMEGP loan can also be applied offline. The applicant needs to find the nearest available KVIC center and submit the offline formand complete the partner bank formalities from which the loan amount is to be disbursed,

PMEGP loan scheme is a facility provided by India’s Government under the KVIC committee to help improve employment opportunities in villages and rural areas. However, entrepreneurs in cities can also apply. The main intent is to help grow employment in the undeveloped parts of India. The loan offers a subsidy ranging from 15-25% depending on the individual’s caste category and has no need to provide collateral to avail the loan. Educational qualification is also not needed if the loan amount is less than 10 lakh and 5 lakhs in the manufacturing and service industries.

It is very much appealing to craftsmen, daily wage workers who get seasonal work and experience tough times finding work throughout the year. Once the loan amount is sanctioned, they also have the option to apply for a second round of funding with the help of other PMEGP connected schemes like MUDRA.